REFERRAL PERKS®

Earn $100* for you and your friend for every successful referral.

Choice is a great thing — especially when it comes to how you budget. Everybody has unique financial needs and goals, which is why it only makes sense to choose a budgeting method that’s tailored to that. Not sure where to start? Here’s a look at four tried-and-true options that are worth considering.

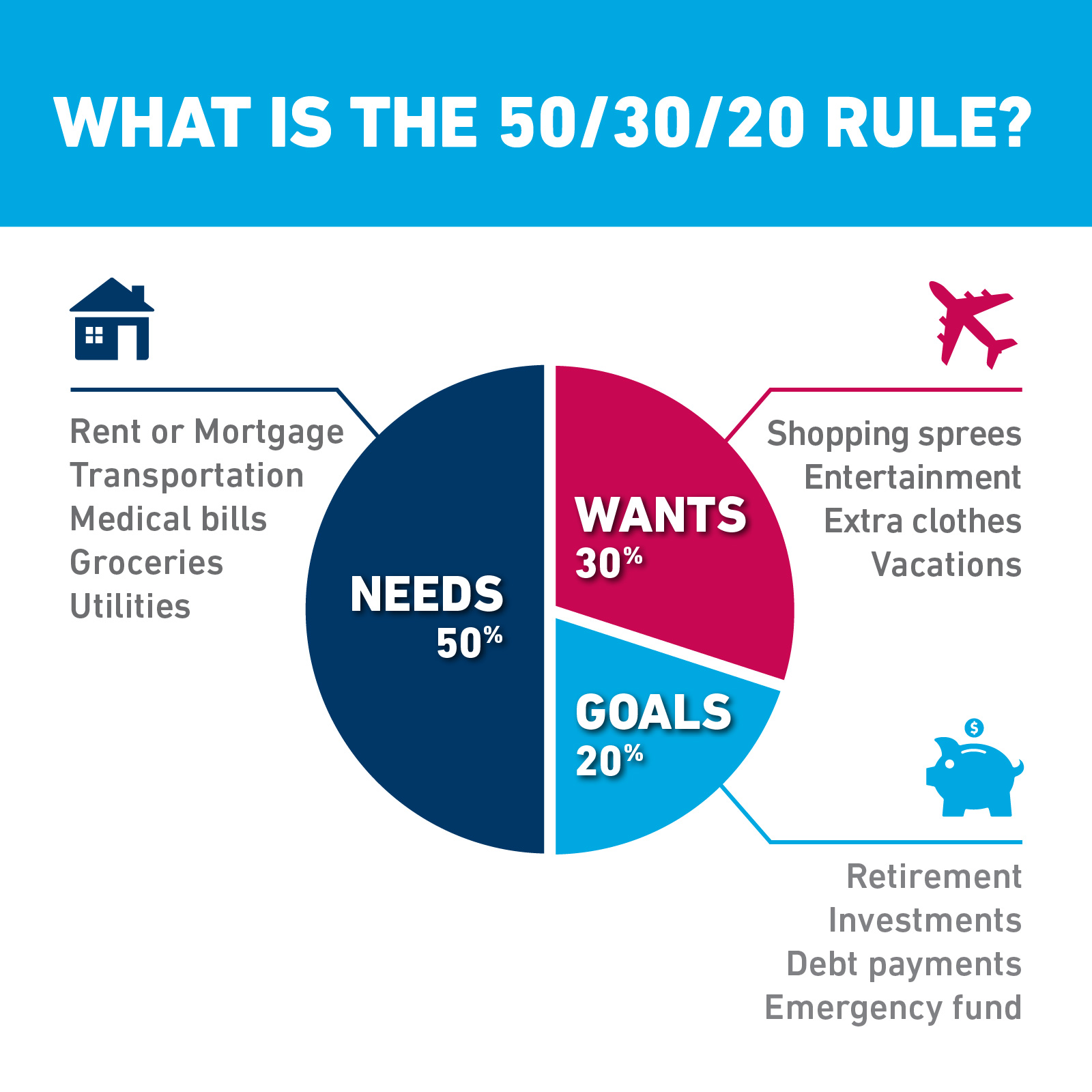

The 50/30/20 method recommends splitting your budget into three simple buckets: needs, wants and savings. After calculating your net monthly income, you’ll allocate 50% to your needs, those bills you absolutely must pay (such as rent, groceries and childcare). 30% to your wants, those things that are not essential (like travel and entertainment). 20% to grow your savings and pay down debt which includes adding or starting an emergency fund or making retirement contributions.

Savings can also include paying down your debt. Minimum payments are parts of needs but paying a little big extra can help you reduce your principal and any extra interest you would pay.

This method is a popular choice among beginner budgeters and those who want a simple, straightforward solution. It’s also best suited for people who have reliable monthly incomes and know how much their take home pay will be each pay cycle.

By helping you thoughtfully balance your spending and saving, the 50/30/20 method can empower you to reach your financial goals.

In zero-based budgeting, every dollar of your income is assigned a job at the beginning of the month. The ultimate task: leave nothing unaccounted for. You’re in the driver’s seat for how you spend your money — so long as your income minus expenses equals zero by month’s end. If your take home pay is $4,000 a month everything you give, save or spend should add up to $4,000. This method may require some more monitoring and course correcting.

Hands-on and detail-oriented budgeters who want to keep close tabs on where their money goes.

Sure, zero-based budgeting can be more time-consuming — but there’s a lot to be gained by being intentional with every single dollar. Plus: This method gives you the freedom to start a fresh budget each month, using your past learnings as a guide.

Also known as the money jar system. With this method, you’ll use cash to pay for your expenses. After you divvy up your net income into your budget categories, withdraw the cash and enclose it in the appropriate envelope or jar. The idea is that you’ll only spend what’s in the envelope each month — nothing more.

Visual learners who tend to overspend and make impulse purchases.

When we pay with cash, we see that cash is truly finite — which can help teach financial discipline.

This approach suggests that you prioritize spending your income on what you care about the most. For instance, do you value travel? Then earmark a larger portion of your budget to that. Is your goal to tuck away money so you’re more prepared for life’s curveballs? Try upping the amount you put in your savings each month. Of course, you’ll need to trim in categories that aren’t as important to you to make that possible.

Those who want to budget, yet still enjoy the things they love in life.

The best budgets are those that don’t feel restrictive. Because this method is personalized to your unique needs and goals, it promotes mindful spending.

There is no one-size-fits-all approach when it comes to budgeting. With a variety of proven methods to choose from, it’s worth investing the time to find the best one for you.

Speak to an advisor on the phone or at a branch.

We acknowledge that we have the privilege of doing business on the traditional territory of First Nations communities.